Argentina was never dollarized

And that's important to keep in mind, notes observatorio argentino 57

Some observers have argued that we know that dollarization would be an absolute disaster because Argentina tried it once, back in the 1990s, and it ended in tears.

It sounds like a compelling argument, but it’s wrong. Argentina never dollarized. What Argentina did do was introduce a new currency (called the peso) at a one-to-one exchange rate with the U.S. dollar. The government guaranteed that exchange rate by requiring that every peso bill in circulation be matched by a dollar worth of short-term U.S. treasuries held by the Banco Central de la República Argentina (BCRA).1

Of course, most money wasn’t backed by BCRA reserves. As they do everywhere else on Earth, private banks issued deposits backed mostly by the banks’ own loans.2 So while the BCRA could change all the pesos in circulation into dollars without breathing hard, it couldn’t change all the peso-denominated deposit accounts in the country into dollars. But that’s a general feature of fixed exchange-rate regimes.

Argentina’s slow crash that started in 1998 (and bottomed out so dramatically in 2001) did not start because of high debt or fiscal laxity. This is important to drive home. Argentina in 1998 was not Greece in 2008. In 1998, Argentine federal debt stood at only 38% of GDP. It was running a small budget deficit of only 1.8% of GDP. Moreover, the Argentine federal government enjoyed what economists call a “primary budget surplus.” That is to say, it was only borrowing to pay interest. That means that all the government had to do to get into the black was to stop paying interest on its debt. Of course, that would mean that nobody would want to lend to it—but if you have a primary budget surplus then you don’t need to borrow!

So what happened? Well, Argentina’s debt was 97% denominated in dollars, whereas the country mostly used pesos. The debt was also growing faster than GDP even with the small deficits, so investors had a reason to be nervous about its future path. Add to that the fact that Argentina was expensive: Argentine exporters were struggling with high costs and Argentine consumers were tempted by cheap consumer goods. So the country ran continual trade (not budget!) deficits that could only be filled by having foreigners buy Argentine assets or lend foreign currency to Argentines.

In 1998. in the wake of big devaluations in Brazil and East Asia, people began to worry that Argentina’s position wasn’t sustainable. So they began to sell their Argentine assets and liquidate their loans to Argentines and get their money out of the country. But the Argentine government (and private Argentines!) still needed to borrow.3 So interest rates rose. But that meant the loans would be harder to pay back. So lenders raised interest rates even more to compensate for the additional risk. But that made the loans still harder to pay back. And as higher interest rates crushed the economy, tax revenues fell. By the time everything fell apart in 2001, the budget deficit had widened to 5.4% of GDP, and now there was a primary budget deficit of 1.3%, so painlessly telling creditors to get lost was no longer an option.

Worse still, people began to expect a devaluation. So nobody wanted to spend dollars that they expected would be worth a lot more in the near future, and nobody wanted to accept pesos that they expected would be worth a lot less in the near future. Anyone who could swapped pesos for dollars and the economy started to slide towards barter. In 2001, it all fell apart. The government devalued, the economy crashed, riots broke out, the President resigned and left office in a helicopter.

Would all that have happened had Argentina used the dollar? We have two obvious counterfactuals: Spain and Greece. Both slid into crisis in 2008; neither had its own currency. How do those two countries in ‘08 compare to Argentina in ‘98?

Well, Greece didn’t look much like Argentina or Spain. The below graph shows budget deficits leading up to and into the crisis.4 The straight vertical line at year zero is the year GDP peaked: 1998 for Argentina, 2008 for Greece and Spain.

Greece was running enormous budget deficits before it ran into trouble. Argentina, on the other hand, went from a small deficit to a medium-sized deficit. It only lost its primary surplus in 2001, when the economy collapsed. Spain ran surpluses until the crisis hit, when it suddenly faced massive deficits. The reason is that Spain’s crisis was similar to Argentina’s in broad strokes (if not in the details). Big capital inflows inflated a housing bubble. When those inflows dried up in the Great Recession the bubble popped and the banks went down with it. The Spanish government didn’t want to see the banks fail, however, because that would have wiped out most Spanish savings and impoverished millions. So it borrowed a fistful of euros and bailed out the banking system.

So what would have happened to Argentina if it had really dollarized? Well, there wasn’t an asset bubble, as in Spain. So while there might have been a banking crisis, it isn’t clear that it would be as bad. Remember, the banking crisis that Argentina actually got had its proximate cause in the growing fear of a devaluation.

But Argentina looked even less like Greece, which had been running massive deficits and suffered a housing bubble.

So, Spain: long grinding stagnation, slow recovery. And Greece: catastophic collapse, followed by worse stagnation.

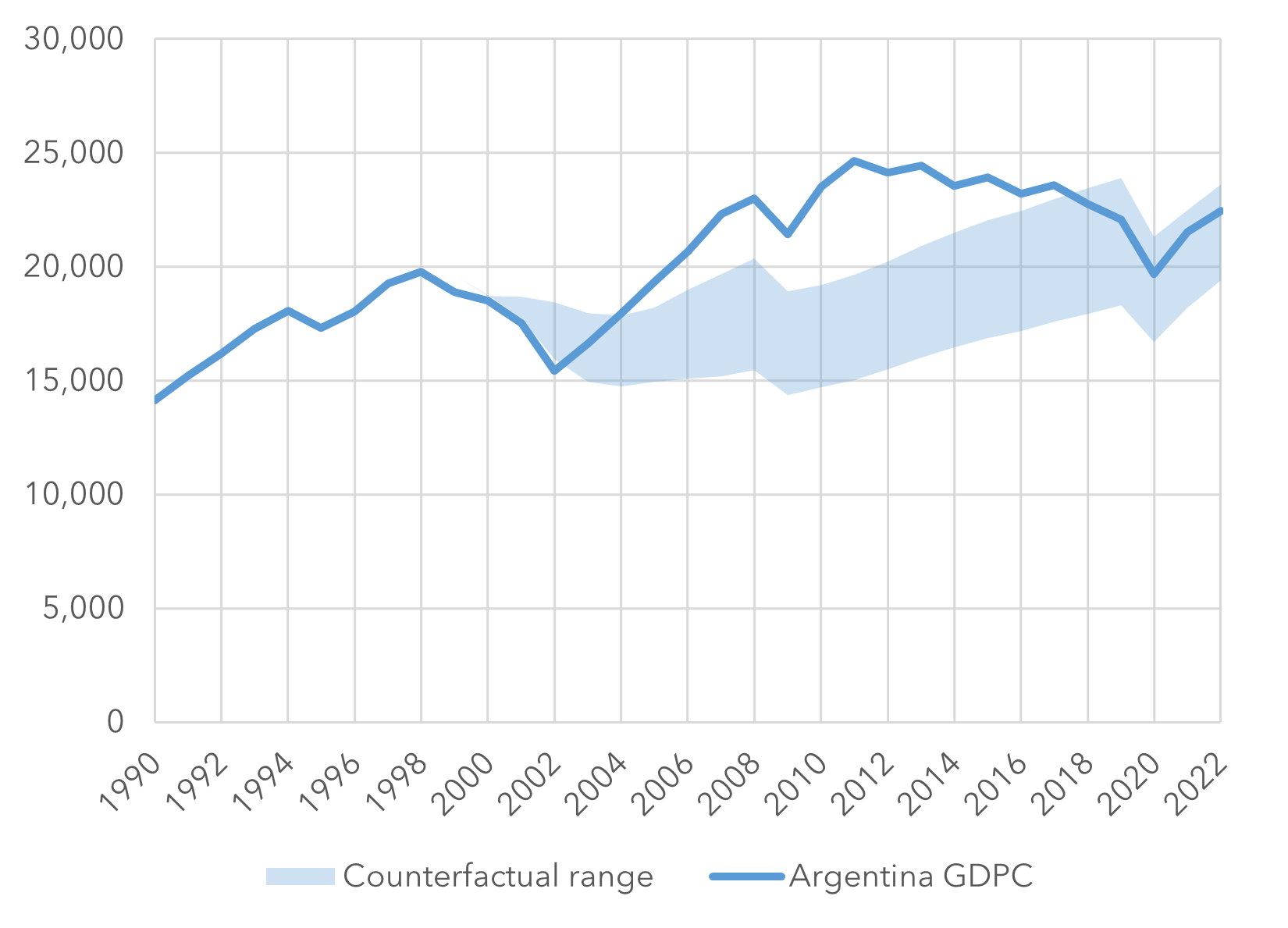

The below chart maps out the possibilities. The vertical axis represents the GDP per capita in U.S. dollars. The blue line shows the path of Argentina’s actual GDP per capita through the end of last year. The top of the lighter blue band traces out a growth path that looks like Spain from 2008 onwards, with a few adjustments that I will explain below. The bottom of the lighter blue band traces out a path that looks like Greece after 2008. You can think of them as the closest we can get to the range of counterfactuals that a dollarized Argentina would have faced.

Here are the adjustments. First, I assumed that counterfactual Argentina would have a baseline growth rate of 2% after 2011, adjusted for changes in the terms of trade. Second, since Argentina was the beneficiary of a spectacular commodity boom in 2003-12, I adjusted its GDP growth upwards by roughly half a percentage point in those years.5 Finally, the recessions in 2008 and 2020 had entirely external origins, so I threw the counterfactuals out the window and reduced GDP by the amount that it actually fell in both years.

If you believe that Argentina would have hit a banking crisis, imposed draconian capital controls, received massive IMF bailouts, and then neither default nor re-introduce the austral, well, then you believe that the lower bound of that band is realistic. In practice, that would mean a terrible scenario of continuing double-digit unemployment, mass poverty, and no sustained growth until 2010. Could Argentina’s social fabric handle something like that? It would be a much worse outcome than the roller-coaster ride the country actually went on after 2001.

But that seems unlikely. Greece’s crisis had roots in astonishing fiscal irresponsibility and capital markets blindly willing to finance it. That looks nothing like Argentina. If Argentina had used the dollar, rather than a peso tied 1:1 to the dollar, then there would have been little fear of a devaluation. It is possible that the government might have eventually defaulted, as it did in the real world, but with a primary surplus the only problem with default would have been the risk of bank runs. But that can be prevented: dollarization didn’t stop Ecuador from defaulting in 2008. And again in 2020.6 Ecuador has banks; they didn’t fail.

Growth in dollarized Argentina would have been slower than the actual 2002-08 boom, since the country wouldn’t be able to devalue. But there would have been growth because the commodity boom still would have happened and it still would have been epic:

Would a scenario along the top of the light blue band have been better than what really happened? It’s hard to say. The recovery would have been slower and more painful—income levels wouldn’t have recovered until 2012, fourteen years after the onset of the depression. But Argentines would not have seen their savings wiped out, and the country would be growing solidly rather than staring down hyperinflation today.7

I think that critics who write that dollarization is a bad idea today because it failed after 1998 are wrong, simply because Argentina never dollarized and the crisis that it did have depended on the existence of a peso with a fixed exchange rate.

But saying that dollarization might have worked in 1998 is also very different from saying that it would be a good idea in 2023. The 1998 crisis was bad luck. Countries all around the world were running into currency crises, leaving the Argentine peso overvalued. And then investors panicked, because the country had a bad reputation and they feared other investors would panic. It was the national equivalent of a bank run, with the unfortunate President de la Rúa in the position of George Bailey.

The current crisis does not look anything like 1998-2001. Argentina doesn’t need to dollarize to get out of its current mess. Moreover, dollarization will be difficult, to put it mildly. It’s almost certainly not a good idea, at least not until the situation is stabilized.

But the reason dollarization is not a good idea now has nothing to do with the experience of the 1990s. Lessons from history are well and good: we tried to draw some in this post. But you need to be sure that the history actually happened.

The Argentines kind of violated the latter, by letting one-third of BCRA reserves be in Argentine federal bonds, not U.S. federal bonds.

By 1998, about 55% of bank deposits were denominated in dollars, up from about a third at the beginning of the currency board in 1991. of That already is a sign that people didn’t really trust the peg! Peso deposits paid higher interest yet every year a higher share of depositors preferred what they thought was the protection of a dollar account. (For data, see page 36 of this IMF report creatively entitled “Lessons from the Crisis in Argentina.”)

The government wasn’t quite ready to stiff creditors in 1998.

Data is from the IMF, which uses standardized measures. The Greek data are the real books, not the cooked ones that the country was caught reporting. Argentine data is reliable for this period.

I actually did something that sounds slightly more sophisticated but really isn’t: I took the estimates from the calibrated model in this paper seriously, and added (or at times subtracted) them from the counterfactual growth rates. I then double checked against estimates in this paper. It doesn’t really get you a much different result from just adding 0.5% to growth every year.

To be fair, the second default involved a lot less angry aggressive rhetoric than the first. I was there for the first one. Ah, memories.

The Argentines also could have floated the peso in 1998 and maybe that would have been even better than dollarization! All I can say is that the country in real life managed to get the worst of both worlds.

What's up Noel. Currently in Argentina right now. I'm working on a job site, and yesterday... every single one of the engineers here supported Milieu. They are just fed up with the system.

I've been reading about dollarization lately, and I see a lot of pro and anti-articles. The one thing I don't see among the anti-dollarization articles is a realistic path forward. What policies could they take that could tame inflation?

My take is no matter what happens, status quo, dollarization, fiscal constraint, there is going to be mass social upheaval.

The engineers I work with advocate for dollarization because they assume that like in the 90s even if Argentina did get things under control, they would just backslide again. There is literally no faith in the government or institutions to behave responsibly. Their support for dollarization is basically their way of advocating breaking the system completely to restart a new.