America will be okay if Trump goes ahead with his tariffs on Mexico

It’s still a terrible idea!

Today the inestimable Latin American Risk Report published a piece stating that President Trump would ruin the U.S. economy if he followed through on his plan to impose a blanket 25% tariff on Mexico.

The tariff is a bad idea. And the President-elect phrased his announcement as the opening shot in a negotiation, so it probably won’t happen fully. But even if it did, it wouldn’t cause the U.S. economy to collapse. It is bad for General Motors, but only slightly annoying for America.

TLDR

There are too many countervailing forces for tariffs to collapse the American economy.

The big one is the exchange rate. The peso was 25 to the dollar not long ago — it then rose to 16 and the world did not collapse. That is the same as a 36% hike in the Mexico cost, at least from the POV of an American importer. Even if you think that businesses pass on only a fifth of exchange rate changes, that’s a 7% tariff change within recent memory. Given that a 25% tariff would likely mean a 12% rise in Mexico costs, we’re not talking about something outside all business experience.

Much of what Mexico sells the United States has a domestic equivalent, especially in the automotive sector. So if prices rise for Mexican inputs, some of that demand will get redirected to domestic producers. That’s sort of the point of the tariffs, actually.

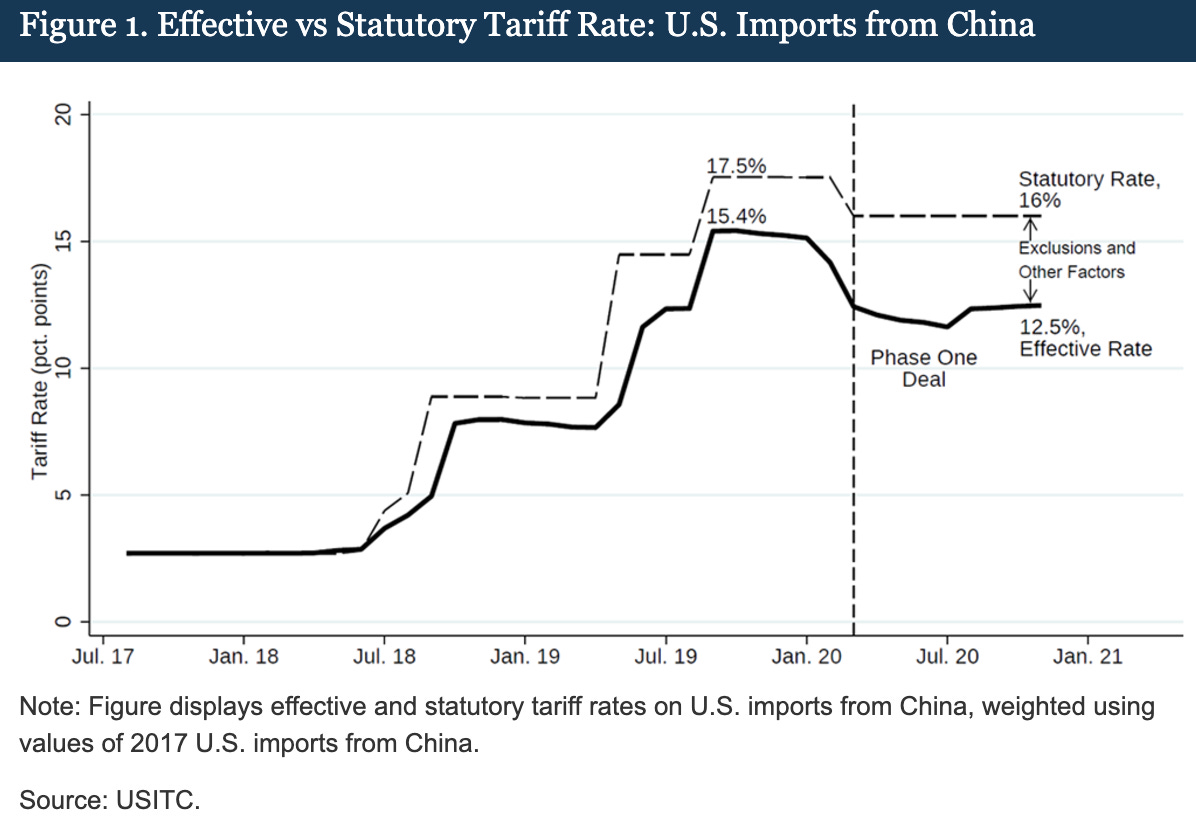

We recently imposed a big tariff hike on most Chinese goods, and the U.S. economy did just fine.

Put it all together and you don’t have much of a case for tariffs of Mexican goods — but the argument that imposing them would ignite a big American recession isn’t very strong. (As opposed to a big Mexican one!)

Here’s a bit more detail.

How tariffs work, or don’t

Tariffs impose taxes on product sales across border. So if the U.S. imposes a 25% tariff on Mexican exports, then it’s the equivalent of imposing a 25% sales tax on purchases from Mexico.

But there are mitigating factors!

Exchange rate effects

If you impose a big tax on purchases from Mexico, then people will want to purchase less from Mexico. Mexican producers ultimately need pesos to pay their workers, rent, power bills, and domestic suppliers. So when they earn dollars from U.S. sales, they sell most of those dollars for pesos.

If Mexican producers sell less to the United States because of the tariff, then they have fewer dollars to swap for pesos. Fewer dollars chasing pesos —> a lower price for the peso, just as fewer dollars chasing pizza would mean a lower price for pizza. (Yes, I’m eating a very good pizza right now. Fazio’s, in Brooklyn. Go try it, it’s great!)

A lower price for the peso is another way of saying that a dollar will now buy more pesos than before. So Mexican producers now need fewer dollars to pay their production expenses. That means they can cut the price they charge American customers to try to keep market share despite the tariff hit.

That said, in practice the exchange rate shift cancels out only part of the impact of tariffs. How much? Well, we don’t really know. Olivier Jeanne and Jeongwon Son (Johns Hopkins) construct a model and calibrate it using data from the U.S. and China. It’s a bit hard to extract a simple number from their work, but one-third is a good enough approximation.

OK, so if DJT slaps on 25% tariffs, the peso “should” slide around 8%. But that seems much too low, no? After all, the peso is currently around 20 pesos per dollar—it’s already fallen 20% since June!

The peso was briefly at 25 after Covid hit, and it’s hard to believe that it wouldn’t fall to at least that level if the Trump administration announced tariffs of 25% on Mexico. In theory, that would totally cancel out the effect of the tariffs.

Pass-through

In practice, not so much. When exchange rates change, sellers don’t pass it all onto buyers. Rather, they enjoy excess profits when their currency falls, and suck up the losses when it rises. The reason is simple. Most buyers and sellers aren’t trading something like wheat in a liquid market. Rather, they have relationships that they’re locked into. It’s a royal PITA to change suppliers or find new customers. Both sides of the transaction know that, so they don’t pass on every single cost bump to each other.

In 2021, Alberto Cavallo, Gita Gopinath, Brent Neiman, and Jenny Tang asked how much do companies pass on changes in tariffs and exchange rates onto their customers? They used BLS data to examine the import prices of Chinese goods affected by new U.S. tariffs compared to those that were not. Then they analysed “millions of online prices from two large multichannel retailers for which we have detailed information on the country of origin and harmonized tariff schedule (HTS) code classifications at the individual product level.” So they could see what happened to the price importers paid and the prices American consumers ultimately paid.

They found that Chinese exporters passed on about 94% of the tariff costs to American wholesale buyers. On the other hand, they also found that Chinese firms pass on only about 20% of the savings from exchange rate depreciations. That’s in line with what Enrique Martínez and Braden Strackman found for Mexico, using a different methodology.

So a 25% tariff hike that produced a 25% drop in the value of the peso would net out to about a 18% jump in wholesale import prices from Mexico. And that’s, well …

We’ve been here before

… just a little bit more than the tariffs we imposed on most Chinese goods back when the trade war started.

The American economy survived.

Why did it survive? Well, let’s turn back to that paper by Cavallo, Gopinath, Neiman, and Tang. They found that almost none of the cost hikes from U.S. tariffs (or savings from the depreciation of the renminbi) were passed on to consumers! Rather, wholesalers ate most of it. I want to repeat that — when you dig into actual price data, almost none of the costs were passed on to consumer.

They do lots of fancy econometrics, but here’s basically how they came to that conclusion. First, they looked at prices changes for products effected by the tariffs versus products that were not. (That’s the panel on the left below.) Second, they looked at the prices of identical products in the United States (which imposed tariffs) and Canada (which did not). Here are the results:

Not much change between the two lines.

Now, hitting Mexico over the head with tariffs would be worse for at least one big industry, because American car manufacturing is totally tied up with Mexico. (And let’s not mention Canada.) That would be bad! Nobody wants the cost of making a car to rise by $3,000. But a rise in new car prices isn’t the same thing as economic destruction. Especially since not all American-based manufacturers have major Mexican operations and there are U.S.-based options to substitute for Mexican inputs.

In addition, I can’t imagine that inasmuch as the car companies run integrated cross-border operations that they won’t pass along all the savings from exchange rate depreciation to themselves. I mean, what else would they do with the savings?

The appeal process

Finally, American trade law offers companies temporary relief from trade measures taken under Section 232 of the Trade Expansion Act of 1962 and Section 301 of the Trade Act of 1974. The president can grant Section 232 waivers on grounds of national security, a lack of domestic suppliers for a particular product, or an inability to get the product domestically in sufficent quantities. Meanwhile, the government can grant Section 301 waivers simply to mitigate “harm to the business.”

I predict with 100% probability that even if the Trump administration goes ahead with massive tariffs on Mexico (and Canada) he will not make it hard to get a 232 or 301 waiver on a temporary basis. That would ease the burden on American firms.

Hysteresis

Eggs are hard to unscramble. Tariffs and transport costs are not the only trade costs! Total trade costs come to the difference in the markup between the factory gate and the final consumer between domestic goods and imported goods. When Dennis Novy (Warwick) used that approach (albeit indirectly) he found that NAFTA reduced the total trade cost between Mexico and the United States from about 70% to around 33%. (Page 10.)

How did that happen? The intuition is as follows. Signing NAFTA cut U.S. tariff rates from 3% to zero. Companies then established cross-border value chains. Those chains were not easy to set up, but once they were in place, it became far cheaper to export. Think of it this way: the first autoparts factory to open up in San Luis Potosí needed to figure out everything about selling to the United States. The fifteenth had a much easier time. Thus, NAFTA caused trade costs to drop by way more than the fall in tariffs.

The flip side of that, however, is that much of the fall in trade costs is not reversible. Abolishing the USMCA and dumping on an effective 12% tariff might have remarkably little effect, taking total trade costs up from 33% to only 45%, which is still rather less than in the days before NAFTA.

As I wrote in 2017, a straight-up tariff in the 20%+ zone would start to undo economic integration in North America. But it wouldn’t be overnight.

Tough on Mexico, tough on the causes of … Mexico?

If Trump goes ahead with the tariffs, they will be terrible for Mexico. A currency depreciation makes anything traded on international markets more expensive, which will reduce Mexican living standards. I also suspect that more of the tariff cost will fall on Mexican producers compared to Chinese ones, if only because many Mexican companies are locked into specific American buyers. (What are you gonna do, sell your alternators to some other auto manufacturer on short notice?)

Moreover, while it would be stupid and counterproductive for Mexico to retaliate, but I can’t imagine the Sheinbaum administration failing to try to punish the United States. If they’re smart, they’ll limit the retaliation to American final goods, you know, U.S. products that go straight to consumers. If they’re stupid, they’ll hit imports of American components for Mexican exports.1

And the tariffs won’t be good for the United States. The auto industry will be hit hard, especially if the tariffs are collected every time an intermediate input crosses the border. (I will try to write a separate piece on that this week.) Maybe a few American producers of some niche products will benefit, but not many. So tariffs on Mexico is a bad idea.

But what it won’t be is an economic catastrophe for the United States.

Back over to you, Boz!

In 2019, Alonso de Gortari calculated that 30% of the headline value of Mexican manufacturing exports to the U.S. consists American exports to Mexico.